Every year Warren Buffett (the Oracle of Omaha) writes a letter to the shareholders of Berkshire Hathaway. It is an occasion eagerly awaited by both investors and the press. Contained in the letters is the usually practical wisdom that he has gained over a lifetime of work starting when he worked at his grandfather’s grocery store through to being the second richest man in the world today.

Over the weekend I read his most recent letter and am highlighting here some of the passages that struck me.

Warren Buffett opens his 2014 letter with this sentence:

Berkshire’s gain in net worth during 2014 was $18.3 billion, which increased the per-share book value of both our Class A and Class B stock by 8.3%.

Lesson:

You should know where your company stands financially at all times. You cannot be an effective decision maker without that knowledge.

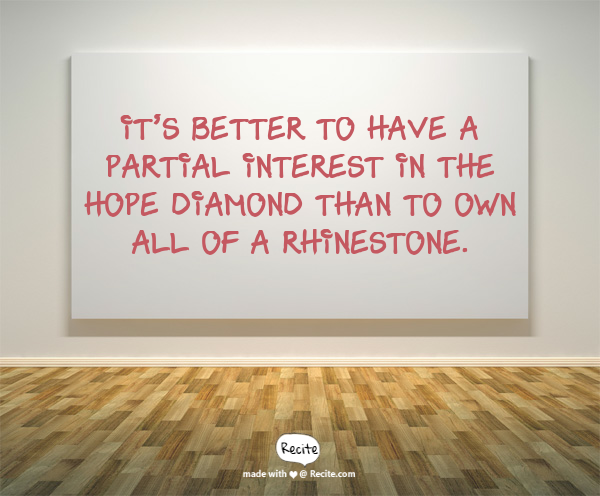

At Berkshire, we much prefer owning a non-controlling but substantial portion of a wonderful company to owning 100% of a so-so business. It’s better to have a partial interest in the Hope Diamond than to own all of a rhinestone.

Lesson:

There are two different lessons I can pull from this statement. The first is that an entrepreneur or business owner should be careful about spreading themselves across multiple entities. If any are struggling then you should consider cutting your losers and doubling down on your winners.

The second is that as an employee you are all in on whatever business you choose to work for. Make sure that it is a diamond.

Berkshire’s great managers, premier financial strength and a variety of business models protected by wide moats amount to something unique in the insurance world. This assemblage of strengths is a huge asset for Berkshire shareholders that will only get more valuable with time.

Lesson:

A great business is comprised of great employees, a great balance sheet, and a business model that allows it to lead an industry and would be hard for competitors to duplicate.

Indeed, borrowed money has no place in the investor’s toolkit: Anything can happen anytime in markets. And no advisor, economist, or TV commentator – and definitely not Charlie nor I – can tell you when chaos will occur. Market forecasters will fill your ear but will never fill your wallet.

Lesson:

Debt is leverage that you can use when times are good but can be fatal for your business when times are bad. Avoid it at much as you can.

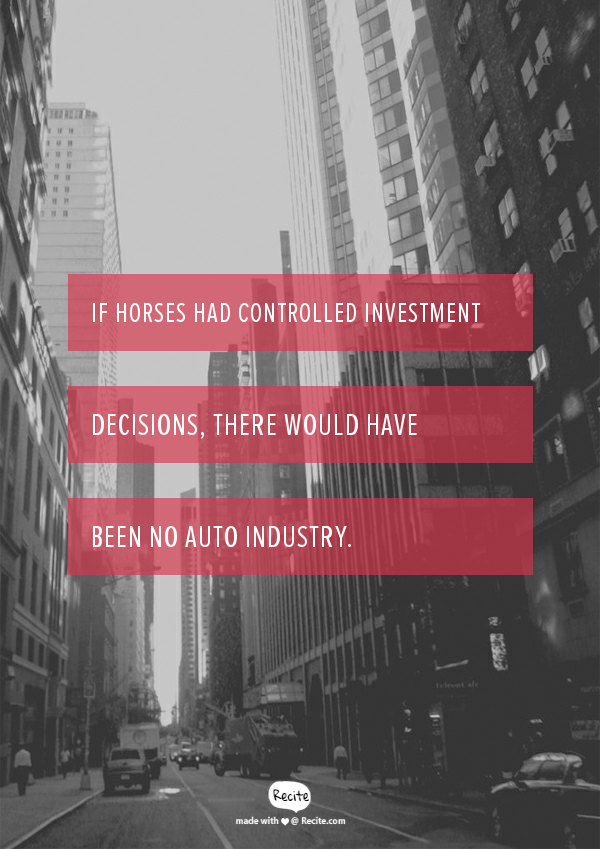

Moreover, we are free of historical biases created by lifelong association with a given industry and are not subject to pressures from colleagues having a vested interest in maintaining the status quo. That’s important: If horses had controlled investment decisions, there would have been no auto industry.

Lesson:

Be wary of colleagues who continuously oppose progress to maintain the status quo. They are looking out for what they (often mistakenly) perceive to be their best interests rather than what is best for the company long term.

Periodically, financial markets will become divorced from reality – you can count on that. More Jimmy Lings will appear. They will look and sound authoritative. The press will hang on their every word. Bankers will fight for their business. What they are saying will recently have “worked.” Their early followers will be feeling very clever. Our suggestion: Whatever their line, never forget that 2+2 will always equal 4. And when someone tells you how old-fashioned that math is — zip up your wallet, take a vacation and come back in a few years to buy stocks at

cheap prices.

Lesson:

By wary of outsiders (consultants, bankers, salesmen, etc.) who promise you things. Nobody knows your business better than you. Once you start walking down the path they are offering it can be hard or impossible to turn back.

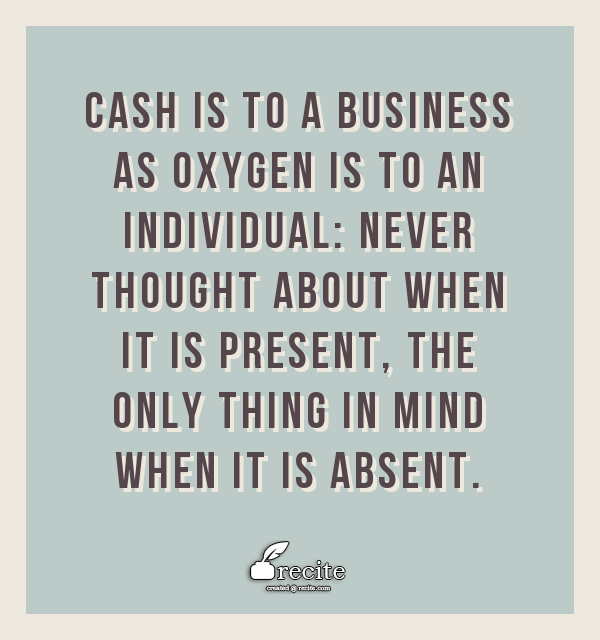

Next up is cash. At a healthy business, cash is sometimes thought of as something to be minimized – as an unproductive asset that acts as a drag on such markers as return on equity. Cash, though, is to a business as oxygen is to an individual: never thought about when it is present, the only thing in mind when it is absent.

Lesson:

Make sure you have cash on the balance sheet. It can serve as a buffer for when your company falls on hard times as well as serve as ammunition for when your competitors are in that position.

The reason for our conservatism, which may impress some people as extreme, is that it is entirely predictable that people will occasionally panic, but not at all predictable when this will happen. Though practically all days are relatively uneventful, tomorrow is always uncertain. (I felt no special apprehension on December 6, 1941 or September 10, 2001.) And if you can’t predict what tomorrow will bring, you must be prepared for whatever it does.

Lesson:

Plan for success. Make sure that plan has contingencies for the inevitable surprises that will occur along the way.

These duties require Berkshire’s CEO to be a rational, calm and decisive individual who has a broad understanding of business and good insights into human behavior. It’s important as well that he knows his limits. (As Tom Watson, Sr. of IBM said, “I’m no genius, but I’m smart in spots and I stay around those spots.”)

Lesson:

A leader should have the 30,000 foot view and be able to delegate effectively. Hire in the areas where you are weak.

My successor will need one other particular strength: the ability to fight off the ABCs of business decay, which are arrogance, bureaucracy and complacency. When these corporate cancers metastasize, even the strongest of companies can falter.

Lesson:

I have a chip on my shoulder for complacency and have personally viewed how it can be a slow, agonizing death of a company. It often does walk hand in hand with bureaucracy and arrogance. Maintain forward momentum through culture and innovation.

All told, Berkshire is ideally positioned for life after Charlie and I leave the scene. We have the right people in place – the right directors, managers and prospective successors to those managers. Our culture, furthermore, is embedded throughout their ranks. Our system is also regenerative. To a large degree, both good and bad cultures self-select to perpetuate themselves. For very good reasons, business owners and operating managers with values similar to ours will continue to be attracted to Berkshire as a one-of-a-kind and permanent home.

Lesson:

Good people coupled with a good culture are what will allow a business to not only endure but to be a succeed as it does so.